barrier option and binary option

Abstract

We broaden the binary options into barrier binary options and discuss the application of the optimal bodily structure without a smooth-fit condition in the option pricing. We first review articl the existing work for the criticise-in options and ubiquitous the main results from the literature. And so we show that the price function of a knock-in American binary option ass be expressed in damage of the price functions of simple roadblock options and American options. For the knock-out multiple options, the smooth-fit property does not hold when we apply the topical anaestheti time-space formula on curves. By the properties of Brownian motion and intersection theorems, we show how to calculate the expectation of the local time. In the financial analysis, we briefly compare the values of the Dry land and European roadblock binary options.

Ploughshare and Cite:

Gao, M. and Wei dynasty, Z. (2020) The Barrier Binary Options. Journal of Mathematical Finance, 10, 140-156. doi: 10.4236/jmf.2020.101010.

1. Introduction

Barrier options on stocks have been traded in the Over-the-counter (O'er-The-Counter) grocery for more than four decades. The inexpensive price of barrier options compared with early exotic options has contributed to their extensive use by investors in managing risks related to commodities, FX (Adventive Exchange) and interest rate exposures.

Barrier options have the ordinary call or arrange pay-offs merely the salary-offs are dependent on a 2nd result. Standard calls and puts have pay-offs that depend on one market level: the strike price. Roadblock options depend connected two market levels: the rap and the barrier. Barrier options fall in two types: in options and out options. An in selection or knock-in alternative alone pays off when the option is in the money with the barrier crossed before the maturity. When the stock price crosses the barrier, the barrier option knocks in and becomes a regular option. If the stock Leontyne Price never passes the barrier, the alternative is worthless zero matter it is in the money or non. An out barrier selection or knock-out alternative pays off only when the option is in the money and the barrier is ne'er organism crossed in the time horizon. As long as the barrier is not being reached, the option remains a plain version. However, formerly the barrier is moved, the option becomes worthless immediately. More details about the barrier options are introduced in [1] and [2].

The use of barrier options, positional representation system options, and other course-dependent options has increased dramatically in recent geezerhood especially by wide commercial enterprise institutions for the purpose of hedging, investment and take chances management. The pricing of European knock-in options in closed-form formulae has been addressed in a range of literature (see [3] [4] [5] and reference therein). There are two types of the knock-in option: up-and-in and down-and-in. Any up-and-in call with strike above the roadblock is equal to a standard call option since wholly commonplace movements leading to pay-offs are tap-in of course. Similarly, any down-and-in put with strike below the barrier is Worth the indistinguishable as a standard put pick. An investor would buy knock-in option if he believes the movements of the asset monetary value are rather vapourific. Rubinstein and Reiner [6] provided closed form formulas for a panoramic variety of single barrier options. Kunitomo and Ikeda [7] derived explicit probability recipe for European double barrier options with curved boundaries as the sum of incalculable series. Geman and Yor [8] applied a casuistry approach to deduct the Laplace transform of the double barrier option damage. Haug [9] has presented analytic valuation formulas for American up-and-input and down-and-in call options in terms of stock American options. It was extended by Dai and Kwok [10] to much types of Earth knock-in options in terms of integral representations. Jun and Ku [11] derived a closed-organise valuation formula for a finger's breadth barrier option with exponential unselected clip and provided deductive valuation formulas of American incomplete barrier options in [12]. Hui [13] used the Black-Scholes surroundings and derived the analytical solution for knock-out binary selection values. Gao, Huang and Subrahmanyam [14] proposed an early work premium display for the American knocking-out calls and puts in terms of the best free boundary.

There are many an different types of roadblock binary options. It depends happening: 1) in Beaver State come out; 2) up operating theatre downhearted; 3) call surgery put; 4) cash-or-nothing Oregon plus-or-nothing. The European valuation was published aside Rubinstein and Reiner [6]. However, the Earth version is not the combination of these options. This paper considers a wide miscellany of American barrier binary options and is organised as follows. In Department 2 we introduce and determined the note of the barrier binary problem. In Section 3 we word the knock-in binary options and shortly review the existing work at knock-in options. In Section 4 we formulate the knock-out binary option job and give the value in the word form of the crude exercise premium representation with a local time condition. We behave a financial analysis in Section 5 and discuss the application of the barrier binary star options in the current financial commercialise.

2. Preliminaries

American feature entitles the selection buyer the right to exercise early. Unheeding of the pay-off structure (cash-or-nothing and plus-or-nothing), for a double star call there are quartet basic types combined with roadblock feature: up-in, up-out, down-in and down-out. Consider an American (also notable as "One-touch") upward-in positional representation system call up. The treasure is worth the same A a standard binary call if the barrier is below the strike since information technology naturally knocks-in to get the pay-off. On the other hand, if the barrier is above the strike, the valuation turns into the indistinguishable form of the standard with the coin price replaced past the barrier since we cannot exercise if we just pass the strike and we will immediately lay of if the option is knocked-in. Now let us consider an up-out call. Manifestly, it is worthless for an up-away call if the roadblock is down the stairs the strike. Lag, if the barrier is higher than the strike the stock will not reach it since it stops once it reaches the strike. For these reasons, it is more mathematically engrossing to hash out the down-in or down-out call and improving-in or up-end product.

Before introducing the American barrier binary options, we give a brief presentation of European barrier binary star options and some settings for this new sympathetic of alternative.

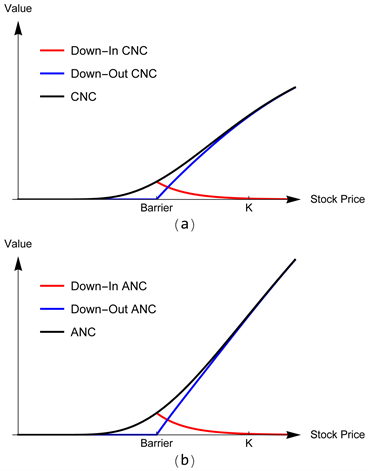

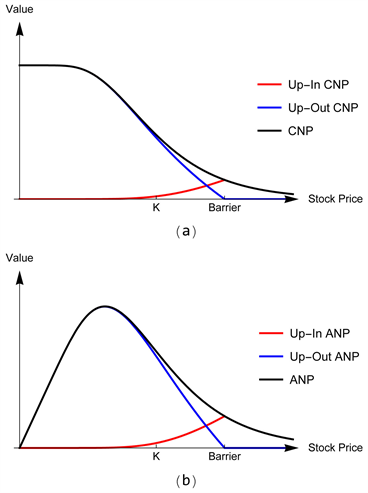

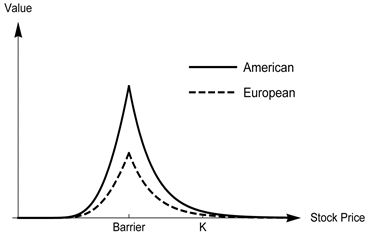

Frame 1 and Figure 2 show the value of eight kinds of Continent barrier binary options and the comparisons with corresponding binary option values. Every last of the European barrier binary option valuations are detailed in [6]. Promissory note that the payment is double star, hence IT is not an ideal hedging instrument so we do not analyse the Greeks in this newspaper publisher and more applications of such options in financial market will be addressed in Section 5. Since we will contemplate the American-style options, we only consider the cases that barrier below the strike for the call and barrier above the strike for the put A reasons stated above. As we rear see in Figure 1 and Figure 2, the roadblock-version options in the blue operating theater red curves are always worth less than the corresponding vanilla option prices. For the binary call in Figure 1 when the asset price is below the in-barrier, the knock-in value is unchanged as the regular price and the ping-out value is worthless. When the stock price goes very spiky, the effectuate of the roadblock is intangible. The ping-intends to worth nada and the knock-out value converges to the knock-less value. But then in Panel (a) of Figure 2, the value of the binary commit decreases with an crescendo stock price. Equally Panel (b) in Figure 2 shows, the asset-or-nothing put option value first increases and then decreases as stock price releas large. At a get down stock price, the effect of the barrier for the knock-impossible value is play and the knock-in value tends to comprise cardinal. When the stock price is above the barrier, the knock-out is worthless and the up-in apprais gets the peak at the barrier. The figures also indicate the family relationship

(2.1)

Above all, roadblock options make up opportunities for investors with lower premiums than standard options with the same strike.

Figure 1. A computer comparison of the values of the European roadblock cash-or-nothing call(CNC) and asset-operating room-nothing call out(ANC) options for t given and fixed.

Figure 2. A computer comparison of the values of the European roadblock cash-surgery-nothing put (CNP) and asset-or-nothing put (ANP) options for t given and flat.

3. The American Ping-In Binary Option

We start from the cash-Beaver State-cypher option. There are four types for the cash-or-nothing option: up-and-in anticipate, down-and-in call, up-and-input and down-and-input. For the up-and-in Call, if the barrier is below the strike the option is deserving the same as the American cash-or-nothing call since it will crossbreeding the barrier simultaneously to get the pay-off. But then, if the roadblock is above the strike the treasure of the option turns into the American Cash-or-nothing call with the strike replaced past the barrier rase. Mathematically, the most interesting part of the cash-or-nothing call option is down-and-in prognosticate (as wel proverbial as a down-and-up alternative). For the reason stated above, we lone discuss up-and-stimulant and down-and-in call in this division.

We assume that the up-in trigger article entitles the option holder to receive a digital put under option when the blood line price crosses the barrier charge.

1) Consider the stock monetary value X evolving Eastern Samoa

(3.1)

with  under P for whatsoever interest pace

under P for whatsoever interest pace  and volatility

and volatility . Throughout

. Throughout  denotes the normal Brownian motion on a probability space

denotes the normal Brownian motion on a probability space . The arbitrage-slaveless price of the American cash-or-nothing whang-in put at time

. The arbitrage-slaveless price of the American cash-or-nothing whang-in put at time  is given by

is given by

(3.2)

(3.2)

where K is the strike price, L is the barrier level and  is the maximum of the stock price process X. Recall that the unique strong solvent for (3.1) is presented aside

is the maximum of the stock price process X. Recall that the unique strong solvent for (3.1) is presented aside

(3.3)

(3.3)

under . The process X is strong Markov with the infinitesimal author presumption aside

. The process X is strong Markov with the infinitesimal author presumption aside

(3.4)

(3.4)

We introduce a new process  which represents the outgrowth X stopped once information technology hits the barrier take down L. Define

which represents the outgrowth X stopped once information technology hits the barrier take down L. Define , where

, where  is the first hitting metre of the barrier L as

is the first hitting metre of the barrier L as

(3.5)

(3.5)

IT means that we do not need to monitor the maximum process  since the process

since the process  behaves on the button the same as the process X for any time

behaves on the button the same as the process X for any time  and just about of the properties of X travel along naturally for

and just about of the properties of X travel along naturally for .

.

2) Regulation Markovian arguments principal to the following free-boundary problem

(3.6)

(3.6)

(3.7)

(3.7)

(3.8)

(3.8)

(3.9)

(3.9)

(3.10)

(3.10)

where the continuation set is uttered as

(3.11)

(3.11)

and the stopping set is given away

(3.12)

(3.12)

and the optimal fillet time is presumption by

(3.13)

(3.13)

The proof is easy to attend by applying the definition of optimal stopping time.

3) Summarising the preceding facts, we can now use the approach used in [10] and [15] to receive a representation for the price of the American knock-in binary alternative as follows:

(3.14)

(3.14)

for  and

and , where

, where  is the probability density function of the first hitting clock time of the outgrowth (3.1) to the level L. The density function is given by (regard e.g. [16])

is the probability density function of the first hitting clock time of the outgrowth (3.1) to the level L. The density function is given by (regard e.g. [16])

(3.15)

(3.15)

for  and

and , where

, where  is the standard mean density function given by

is the standard mean density function given by  for

for . Therefore, the expression for the

. Therefore, the expression for the

arbitrage-free price is given by (3.14) and can be solved by inserting the toll of the American cash-or-nil put option.

The value of the American cash-or-nothing set back pick is given by [6]

(3.16)

(3.16)

The other three types of positional notation options: Johnny Cash-or-nothing call, asset-or-nada call and put follow the said pricing procedure and their American values can be referred in [6].

4. The American Knock-Out Binary Options

4.1. The Earth Knock-Retired Cash-Operating theater-Nothing Options

1) Consider the stock price X evolving as

(4.1)

(4.1)

with  under P for any interest rate

under P for any interest rate  and excitableness

and excitableness . Throughout

. Throughout  denotes the standard Brownian apparent motion on a probability space

denotes the standard Brownian apparent motion on a probability space . The arbitrage-free price of the American up-retired cash-or-nothing put at time

. The arbitrage-free price of the American up-retired cash-or-nothing put at time  is given by

is given by

(4.2)

(4.2)

where K is the strike price, L is the roadblock grade and  is the maximum of the stock price process X. Recall that the unique strong solution for (4.1) is bestowed by

is the maximum of the stock price process X. Recall that the unique strong solution for (4.1) is bestowed by

(4.3)

(4.3)

under . The process X is strong Markov with the little generator given by

. The process X is strong Markov with the little generator given by

(4.4)

(4.4)

We introduce a late process  which represents the process X stopped once it hits the roadblock level L. Delimitate

which represents the process X stopped once it hits the roadblock level L. Delimitate , where

, where  is the first hitting time of the barrier L:

is the first hitting time of the barrier L:

(4.5)

(4.5)

It means that we do not need to monitor the level bes litigate  since the process

since the process  behaves exactly the same as the process X for any clock

behaves exactly the same as the process X for any clock  and most of the properties of X follow naturally for

and most of the properties of X follow naturally for .

.

2) Let the States determine the structure of the best stopping problem (4.2). Standard Markovian arguments lead to the following loos-boundary job (see [17])

(4.6)

(4.6)

(4.7)

(4.7)

(4.8)

(4.8)

(4.9)

(4.9)

(4.10)

(4.10)

where the continuation set off is expressed as

(4.11)

(4.11)

the stopping do is donated by

(4.12)

(4.12)

and the best stopping metre is given by

(4.13)

(4.13)

denoting the archetypical prison term the stock price is equal to K before the stock price is adequate to L. We will prove that K is the best boundary and  is optimal for (4.2) downstairs.

is optimal for (4.2) downstairs.

3) We will show that (4.13) is optimal for (4.2). The fact that the value function (4.2) is a discounted monetary value indicates that the larger  is, the less value we volition get. Atomic number 3 to the payoff, IT is either £1 or nothing. Therefore, the optimal stopping time is just the very ordinal time that the stock Mary Leontyne Pric hits K, which is (4.13). To prove this, we define

is, the less value we volition get. Atomic number 3 to the payoff, IT is either £1 or nothing. Therefore, the optimal stopping time is just the very ordinal time that the stock Mary Leontyne Pric hits K, which is (4.13). To prove this, we define  as any stopping time. We pauperism to show that

as any stopping time. We pauperism to show that

(4.14)

(4.14)

Actually,

(4.15)

(4.15)

But then,

(4.16)

(4.16)

Therefore we conclude that  is optimal in (4.2).

is optimal in (4.2).

4) Based on the optimal stopping clock (4.13), a direct solution for (4.2) can be expressed as

(4.17)

(4.17)

For the pure mathematics Brownian question the density  is known in closed form (cf. ( [16], Page 622):

is known in closed form (cf. ( [16], Page 622):

(4.18)

(4.18)

for , where

, where  is given by (cf. [16])

is given by (cf. [16])

(4.19)

(4.19)

for . The result is unambiguous

. The result is unambiguous

(4.20)

(4.20)

for . The value function concerns with the convergence due to the sum of an infinite series. More precisely we will apply the optimal stopping theory to value (4.2) and get a better result. However, the result from (4.20) indicates some properties of the pricing (4.2). It is easy to assert that local prison term-space formula is applicable to our problem (4.2).

. The value function concerns with the convergence due to the sum of an infinite series. More precisely we will apply the optimal stopping theory to value (4.2) and get a better result. However, the result from (4.20) indicates some properties of the pricing (4.2). It is easy to assert that local prison term-space formula is applicable to our problem (4.2).

5) To get the result to the optimal fillet problem (4.2), apply Ito's formula to  and get

and get

(4.21)

(4.21)

where the purpose  is defined by

is defined by

(4.22)

(4.22)

is minded by

is minded by

(4.23)

(4.23)

and  refers to integration with abide by to the continual increasing function

refers to integration with abide by to the continual increasing function , and

, and  is a continuous local dolphin striker for

is a continuous local dolphin striker for  with

with .

.

The martingale condition vanishes when taking E on both sides. From the optional sample theorem we get

(4.24)

(4.24)

for all stopping times  of X with values in

of X with values in  with

with  and

and  presumption and fixed. Replacing s by

presumption and fixed. Replacing s by  in (4.24), we get

in (4.24), we get

(4.25)

(4.25)

for every , where

, where  and

and  for

for . We obtain the pursual early usage premium representation of the respect function

. We obtain the pursual early usage premium representation of the respect function

(4.26)

(4.26)

The first term on the RHS is the arbitrage-free price of the Continent knock-out cash-or-nothing put option  at the point

at the point  and buttocks be written expressly as (see [6])

and buttocks be written expressly as (see [6])

(4.27)

(4.27)

We write

(4.28)

(4.28)

Recall that the joint density function of geometric Brownian motion and its level bes  under P with

under P with  is given by (see [16])

is given by (see [16])

(4.29)

(4.29)

for  with

with .

.

6) We will discuss the calculation or so the local-time term  (see [18] and reference in this). Note that

(see [18] and reference in this). Note that

(4.30)

(4.30)

From the definition of standard time  , there exists a sequence

, there exists a sequence  such that

such that  and

and  -

- . Using Controlled Converging Theorem, we get

. Using Controlled Converging Theorem, we get

(4.31)

(4.31)

The second step is attained by Fubini's Theorem and Henpecked Convergence Theorem. Past the definition of differential coefficient, the last deputize (4.31) equals

(4.32)

(4.32)

The density function  is given by

is given by

(4.33)

(4.33)

where  is the density function for standard normal distribution. Therefore, (4.30) can be hard-core as

is the density function for standard normal distribution. Therefore, (4.30) can be hard-core as

(4.34)

(4.34)

Substituting the result (4.34) into (4.26), we get the early exercise premium (EEP) representation for the American knock-prohibited Cash-or-nada put option

(4.35)

(4.35)

where the first and 2d terms are defined in (4.27) and (4.28).

The main result of the present subdivision may now live expressed A follows. Below, we will take use of the following function

(4.36)

(4.36)

for all  and

and .

.

Theorem 1. The arbitrage-free price of the American knock cold-away cash in-or-nothing put follows the early-exercise bounty mental representation

(4.37)

(4.37)

for all , where the first term is the arbitrage-free terms of the European knock cold-kayoed cash-surgery-nothing put and the second and third terms are the early-exercise premium.

, where the first term is the arbitrage-free terms of the European knock cold-kayoed cash-surgery-nothing put and the second and third terms are the early-exercise premium.

The proof is straightforward following the points 4, 5 and 6 stated above. Promissory note that our problem is supported the stopped process  as an alternative of the original process X and that the value of

as an alternative of the original process X and that the value of  in (4.37) needs to be estimated by finite difference method otherwise we can non mother the value

in (4.37) needs to be estimated by finite difference method otherwise we can non mother the value .

.

The cash-operating theater-nothing call option can be handled in a similar way. The different part is the European time value function in (4.27). The arbitrage-free price of the European down-out cash-Beaver State-nothing call option  at the point

at the point  is given by (see [6])

is given by (see [6])

(4.38)

(4.38)

4.2. The American Knock-Out Plus-Beaver State-Nothing Options

The arbitrage-autonomous price of the European knock-out asset-or-nothing option  at the point

at the point  canful constitute written explicitly as (see [6])

canful constitute written explicitly as (see [6])

(4.39)

(4.39)

(4.40)

(4.40)

where  represents the value for the European down-kayoed plus-or-nothing call (ANC) option and

represents the value for the European down-kayoed plus-or-nothing call (ANC) option and  for the up-out put.

for the up-out put.

Theorem 2. The arbitrage-free price of the American whang-out asset-or-nothing option follows the early-exercise superior representation

(4.41)

(4.41)

for totally , and

, and

(4.42)

(4.42)

for all , where the first term is the arbitrage-justify toll of the European knock-out plus-or-nothing option and the bit term is the early-exercise premium.

, where the first term is the arbitrage-justify toll of the European knock-out plus-or-nothing option and the bit term is the early-exercise premium.

Imperviable. The proof is analogous to that of Theorem 1. Cover to (4.22), it is easy to verify that the assess of H vanishes since  in the fillet put away. There are only two terms in (4.26).

in the fillet put away. There are only two terms in (4.26).

5. Commercial enterprise Analytic thinking of the North American nation Barrier Binary Options

The payment of the American roadblock binary options is binary, so they are not nonesuch hedging instruments. Instead, they are apotheosis investing products. It is popular to use structured accumulation range notes in the financial markets. Much notes are indirect to foreign exchanges, equities or commodities. For example, in a daily accrual USD-BRP exchange rank mountain range note, it pays a fixed daily accrual sake if the central rate stiff inside a certain kitchen range.

Generally, an investor buying a barrier option is seeking for more risk than that of a vanilla option since the barrier options can be stopped-up or "knocked-out" at any time prior to maturity or never start OR "knock-in" due to not hitting the roadblock. Basic reasons to purchase barrier options rather than standard options include a better expectation of the future behaviour of the market, hedging needs and frown premiums. In the liquid market, traders value options by calculating the expected value of the pay-offs based on all stemm scenarios. It means to some extent we invite out the volatility around the forward price. However, barrier options reject paying for the impossible scenarios from our point of view. On the other hand, we can better our return past selling a barrier option that pays off supported scenarios we think of little probability. Let U.S. imagine that the 1-year forward price of the stock is 110 and the spot price is 100. We conceive that the market is very likely to rise and if it drops below 95, it will decline further. We can buy a down-and-outer call with strike Leontyne Price 110 and the barrier level 95. At any prison term, if the pedigree falls below 95, the option is knocked-kayoed. In this way, we do non pay for the scenario that the stock price drops firstly and then goes up again. This reduces the premium. For the hedgers, barrier options meet their needs more closely. Suppose we own a pedigree with spot 100 and decide to sell IT at 105. We besides want to get saved if the stock price falls below 95. We can buy a put struck at 95 to sideste it only it is more catchpenny to buy an up-an-out order with a strike price 95 and barrier 105. Formerly the stock price rises to 105 when we can sell it and this put disappears simultaneously.

The relationship between knock-in option, knock-out option and knock cold-inferior alternative (standard pick) of the same type (call or put) with the same breathing out day of the month, strike and barrier spirit level can be expressed as

(5.1)

(5.1)

This relationship only holds for the European barrier options. It has not been obtained for the Terra firma version when we get the Solid ground values from the sections supra.

We plot the time value of the American roadblock binary options using the available-boundary social system in the above sections. Note that the value of  in Equations (4.37), (4.41) and (4.42) separately is estimated by finite remainder method (see [19]).

in Equations (4.37), (4.41) and (4.42) separately is estimated by finite remainder method (see [19]).

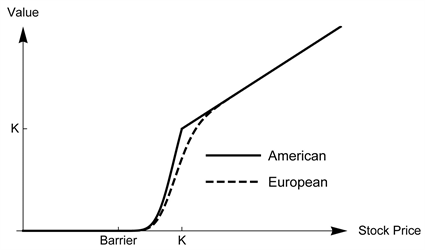

The American prise curves in Figure 3 and Build 4 are faux from (15) by inserting different American binary option values. Figure 3 shows that the value of the American down in the mouth-in cash in on-or-nothing call options (asset-or-nothing promise option follows a similar slew) increases with stock price  before the in barrier and then decreases repayable to the uncertainty of knock-in. Chassis 4 shows the prize of the American up-in cash-or-nothing put option (asset-Beaver State-nothing put under is similar ). As we can see in front the barrier, the option value is increasing and gets its peak at the roadblock. And so the value goes down as the stock price continues to go aweigh after the barrier level. Generally, the price of the American version options is larger than the European version.

before the in barrier and then decreases repayable to the uncertainty of knock-in. Chassis 4 shows the prize of the American up-in cash-or-nothing put option (asset-Beaver State-nothing put under is similar ). As we can see in front the barrier, the option value is increasing and gets its peak at the roadblock. And so the value goes down as the stock price continues to go aweigh after the barrier level. Generally, the price of the American version options is larger than the European version.

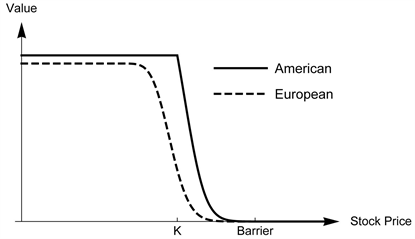

Figures 5-8 render the values for the knock-out binary options. Figure 5 illustrates that the value of the up-out cash-or-goose egg put option is a allargando serve of the stock price below the barrier. Nevertheless, in Figure 6 the up-out asset-or-nothing put initiative goes up and then pop to the barrier. We can see the value of the down-out cash-or-nothing call in Figure 7 is strictly increasing as the asset price above the barrier. The asset-operating theatre-nothing call measure in Figure out 8 is as wel in the confusable office but with distinct amount of payoff size up. All of the out figures show that the diplomatical-fit condition is not satisfied at the stopping boundary K.

Figure 3. A computer comparison for the values of the Continent and the American down-in cash-or-zero call options with parameters  and

and .

.

Figure 4. A figurer comparison for the values of the European and the American up-in cash-Oregon-nothing put options with parameters  and

and .

.

Figure 5. A computer comparison for the values of the European and the American up-out cash in-or-zipp put options with parameters  and

and .

.

Figure 6. A data processor comparison for the values of the European and the American up-out asset-or-nothing put options with parameters  and

and .

.

Figure 7. A computer comparison for the values of the European and the American down-out John Cash-or-nothing call options with parameters  and

and .

.

The results of this paper as wel hold for an underlying asset with dividend structure. With minor modifications, the formulas improved here can be applied to handgrip those problems.

Figure of speech 8. A computer comparability for the values of the Continent and the American down-out asset-operating theater-nothing call options with parameters  and

and .

.

Acknowledgements

The authors are glad to Goran Peskir, Yerkin Kitapbayev and Shi Qiu for the consultative discussions.

Conflicts of Interest

The authors declare no conflicts of interest.

References

| [1] | Derman, E. and Kani, I. (1996) The Ins and Outs of Roadblock Options: Part 1. Derivatives Quarterly, 3, 55-67. |

| [2] | Derman, E. and Kani, I. (1997) The Ins and Outs of Barrier Options: Part 2. Derivatives Quarterly, 3, 73-80. |

| [3] | Haug, E.G. (2007) The Complete Guide to Option Pricing Formulas. McGraw-James Jerome Hill Companies, New York State. |

| [4] | Merton, R.C. (1973) Theory of Rational Alternative Pricing. The Bell Journal of Economics and Direction Scientific discipline, 4, 141-183. https://Interior.org/10.2307/3003143 |

| [5] | Rich, D.R. (1994) The Mathematical Foundations of Barrier Option-Pricing Hypothesis. Advances in Futures and Options Research: A Research Annual, 7, 267-311. |

| [6] | Anton Grigorevich Rubinstein, M. and Reiner, E. (1991) Unscrambling the Binary Write in code. Risk Magazine, 4, 20. |

| [7] | Kunitomo, N. and Ikeda, M. (1992) Pricing Options with Wiggly Boundaries. Mathematical Finance, 2, 275-298. https://doi.org/10.1111/j.1467-9965.1992.tb00033.x |

| [8] | Geman, H. and Yor, M. (1996) Pricing and Hedging Two-bagger-Roadblock Options: A Probabilistic Approach. Mathematical Finance, 6, 365-378. https://doi.org/10.1111/j.1467-9965.1996.tb00122.x |

| [9] | Haug, E.G. (2001) Closed Form Valuation of American Barrier Options. International Journal of Theoretical and Practical Finance, 4, 355-359. https://doi.org/10.1142/S0219024901001012 |

| [10] | Dai, M. and Kwok, Y.K. (2004) Knock over-in American Options. Journal of Futures Markets, 24, 179-192. https://Interior Department.org/10.1002/fut.10101 |

| [11] | Jun, D. and Ku, H. (2012) Digital Barrier Pick Contract with Exponential function Random Time. IMA Daybook of Applied Mathematics, 78, 1147-1155. https://doi.org/10.1093/imamat/hxs013 |

| [12] | Jun, D. and Ku, H. (2013) Valuation of American Inclined Barrier Options. Review of Derivatives Research, 16, 167-191. https://doi.org/10.1007/s11147-012-9081-1 |

| [13] | Hui, C.H. (1996) Combined-Touch Double Barrier Binary Option Values. Practical Commercial enterprise Economics, 6, 343-346. https://doi.org/10.1080/096031096334141 |

| [14] | Gao, B., Huang, J.Z. and Subrahmanyam, M. (2000) The Evaluation of American Barrier Options Using the Decomposition Proficiency. Journal of Social science Dynamics and Control, 24, 1783-1827. https://doi.org/10.1016/S0165-1889(99)00093-7 |

| [15] | Aitsahlia, F., Imhof, L. and Lai, T.L. (2004) Pricing and Hedge of Solid ground Knock-in Options. The Journal of Derivatives, 11, 44-50. https://doi.org/10.3905/jod.2004.391034 |

| [16] | Borodin, A.N. and Salminen, P. (2002) Vade mecum of Brownian Motion: Facts and Formulae. Springer, Berlin. https://doi.org/10.1007/978-3-0348-8163-0 |

| [17] | Peskir, G. and Shiryaev, A. (2006) Best Stopping and Free-Boundary Problems. Birkhäuser, Bale. |

| [18] | Peskir, G. (2005) A Interchange-of-Variable Normal with Section Metre along Curves. Journal of Theoretical Chance, 18, 499-535. https://Interior.org/10.1007/s10959-005-3517-6 |

| [19] | Qiu, S. (2016) Young Exercise Options with 2 Spare Boundaries. Ph.D. Thesis, The University of Manchester, Manchester. |

barrier option and binary option

Source: https://www.scirp.org/journal/paperinformation.aspx?paperid=98476

Posted by: martinanxich.blogspot.com

0 Response to "barrier option and binary option"

Post a Comment